Opinion

Obligation for a structural change in Russia: How to exit from the oil-gas economy?

By analyzing the past, present, and future of Russia’s two major export commodities, I will discuss the impacts of the current developments on the budget and the inevitable need for changes in its economic strategy in this article.

First of all, one of the key notions below, “distant nations,” needs some background. Whether or not they are members of the Commonwealth of Independent States (CIS), all former Soviet countries are still regarded as close foreign countries. The rest of the world is likewise distant foreign countries. Here, we only do calculations and charts for distant foreign countries. After leaving China out, European countries constituted its overwhelming majority. Therefore, the conclusion will reflect the impacts of Western sanctions on Russia’s two primary exports and sources of budgetary income (oil and natural gas).

Let me state something upfront for the sake of the reader who is not a fan of lengthy writings. Using 2021 as a baseline, Russia will lose 35% – 40% of its oil and petroleum product exports and 50% of its natural gas exports this year. However, this is only part of Russia’s financial setback. Before the onset of the deep crisis in the first half of 2022, rising energy prices had significantly boosted the country’s income. However, the situation has now reversed, with oil and petroleum products discounted by nearly half their market price.

Natural gas

We’ll begin by explaining how the graph below was drawn, which data was utilized how and why, and how estimations were made.

In order to avoid “misjudgments, speculations, and inconsistencies,” the Federal Customs Administration (FCA) has not released information since April. Hence there is currently no official data for 2022. Gas exports to Europe (in transit via Ukraine) are projected to reach 30 bcm in 2023. At 80% capacity, gas is plummeted through Blue Stream, which equals a maximum of 16 bcm through this line. The largest volume that can be plummeted to China is between 23 and 24 bcm.

It was not disclosed how much natural gas Turkey purchased from Russia last year. However, on July 18, Yuri Ushakov, an advisor to Putin, reported that 12.8 bcm of gas (7.1 Blue Stream, 5.7 Turk Stream) had plummeted in the year’s first half. In addition, the export amounts to China and Europe (excluding “close countries” like the Baltic) are known. Based on these statistics, I estimated the gas export to Turkey at 21.70 bcm. This figure matches what Kommersant reported to the Turkish Customs Administration: 21.50 bcm.

Data from Gazprom and the FTS do not quite match. Gazprom’s export figures are always greater than FTA’s. This also held true in the year 2021. Novak reported on December 28 that Gazprom had exported 185.1 bcm to distant countries. However, according to FTS, total exports to distant countries were 170 bcm. I derived figures on the graph from Gazprom statistics. Additionally, I referred to the Central Bank’s yearly average natural gas prices. Like the FTA, the Central Bank did not integrate the averages of 2022 and afterward into its statistics. Therefore, I utilized the calculations provided by the RIA based on the ICE data as the average natural gas price in 2022: $1260.8 per mcm.

I picked two sets of prices for 2023. First, the price on December 31, 2022, is $844.3, assuming it remains relatively stable throughout the year. If scenario two plays out, temperatures in Europe will remain above seasonal norms this winter and spring, the wind will continue its record-setting speed, Brussels will strike a long-term oil deal with Qatar, relations with Algeria will improve, and the United States will replace the monopoly profit with reasonable prices. Although not all of them are realistic, I would predict that costs can be cut in half if all take place.

For 2023, I have assumed a decline in exports of 30% and a total decrease to 70-75 bcm. If this occurs, European countries will import more than twice as much natural gas from the United States as they did from Russia this year.

Novak said on December 28 that gas exports totaled 100.9 bcm last year. It is a record low. In 1990, it was 110 bcm. On January 16, Miller reported that 15.5 bcm of gas was sold to China. However, Neftegaz announced on January 2 that this figure might be appraised as 18.2 bcm due to an increase in contractual obligations. The graph relies on this second figure.

Miller also said annual gas shipments to China will reach 48 bcm by 2025. But the graph shows that even in this case, the demand from the East cannot make up for the European market loss (at least for now).

I have omitted liquefied natural gas (LNG) from the charts. This export may increase partially. Nearly 16 million tons of LNG were sent to Asia in 2022, and Europe received 15.7 million tons in total. This amount is approximately equal to 44 bcm of gas. Although this figure is not inconsequential, it is not anticipated to increase beyond this level in 2023 owing to the challenges of insurance-reinsurance in transport and tankers other than dependency on Western technology. Furthermore, it is unlikely that the rise in LNG exports would come close to replacing the 180-200 bcm of the potential capacity of the Russia-Europe pipelines before NATO destroyed Nord Stream 1 and 2.

Even by an optimistic prediction, the total demand of China, Belarus, and Turkey in 2023 would only amount to 60 bcm, less than a quarter of Gazprom’s entire supply capacity. So, this is the picture based on the most optimistic estimates: In 2021, Russia globally sold almost 240 bcm of natural gas. By 2023, however, it will only be able to ship a maximum of 45 bcm LNG and export 30 bcm via pipeline to “unfriendly” countries and 60 bcm to neutral countries.

Oil

Let’s look at oil.

I will prepare the chart for the same time frame (2013-2023); however, I will be excluding the data from China, Turkey, and India. For these three reasons:

1) There are gaps in the dataset. On the bright side, it is at least evident that China had been a reliable purchaser (between 70-72 million tons) until 2022.

2) At least as of 2020, Turkish and Russian sources contradict in terms of figures for Turkey’s purchases.

3) Prior to 2022, India was not a huge market for Russian exports, but after that year, it became one of the most important hubs for Russian oil. The share of Russian oil export to India rocketed from 1% on February 24 to 18% in May. India, Turkey, Singapore, and even the United Arab Emirates (UAE) dilute Russian oil before being sold to obfuscate its origin. It is unclear, however, how they would act after Russia’s counter-sanctions go into effect on February 1. Thus, qualifying the data of these three countries will not provide useful insights.

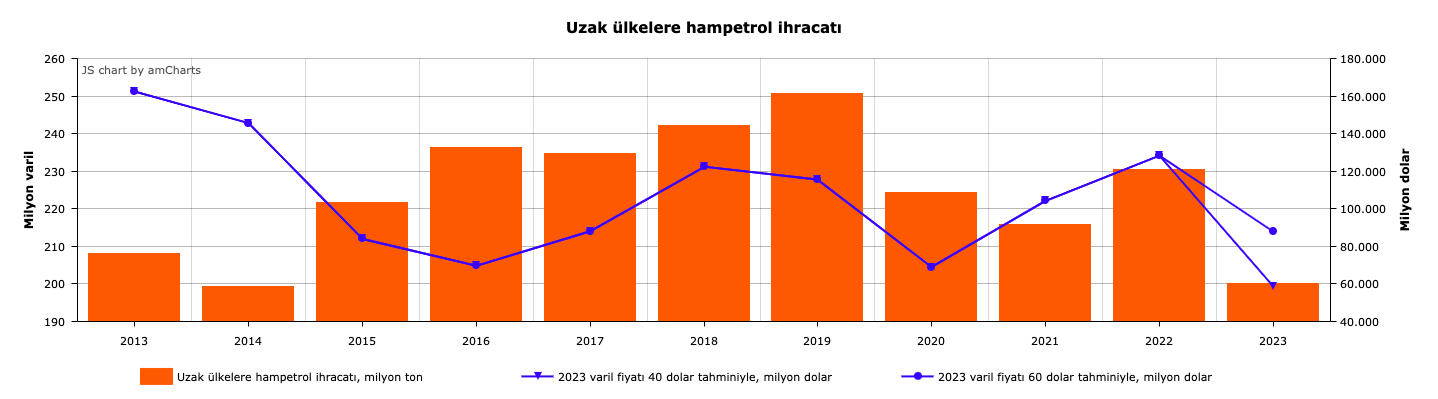

Nevertheless, we may get insights from the figures of crude oil exports and the total income of the annual average oil price.

Like natural gas, I have completed the chart relying on the data of “distant countries” and my own estimates. Similar to natural gas, I predicted a range of $40 to $60 for the barrel price of Ural oil in 2023. These predictions align with the scenarios the Central Bank announced in May. Considering the $60 maximum price, the likely range for the price of Ural oil is between these two extremes. To “distant countries,” I projected 200 million tons of oil exports in 2023. As a result, Russia will lose 90% of its crude oil exports to Europe due to the sanctions, which may cost the country $40 to $70 billion.

I will not go into technical details of the implementation of the sanctions and embargo. Still, it’s important to know that in its broadest sense (including both land and sea traffic), it will be implemented over the course of 6-8 months. This is why the European market has not been totally lost: Bruegel, a European think tank, has shown that 75% of Russia’s oil and petroleum product exports to Europe are sent offshore, while just 25% are transported via pipeline. Germany and Poland, two main consumers, have reduced their purchases, while the Hungarian government has blocked a full ban. Orbán has ensured that the oil pipelines of Slovakia and the Czech Republic from Russia, in addition to those of Hungary, will remain open.

However, the insurance and reinsurance restrictions directly impact exports to India and China. Unless a stable solution to this issue is found (a partial solution is already available; the Russian National Reinsurance Company carries out the reinsurance), overall exports may fall further. Similar to natural gas, compensating the European market with Asia cannot happen in one day.

My estimations for potential losses are in line with these predictions as well. AlfaBank reported an expected loss of $50 billion; for Reuters, it is $40 billion to $54 billion, and for Energy Aspects, $60 billion. Increasing the amount of oil exported may improve the situation, which is feasible if the methods to circumvent the sanctions are broadened. A significant increase in the $40-$60 range for the sale of Ural oil appears unlikely.

These two charts depict a very critical scenario for 2023: Excluding petroleum products and LNG, we may expect Russia’s oil and natural gas income to be between $89.3 and $149.4 billion. This means a revenue drop of between $106 and $166 billion compared to the previous year.

Budget

Budget revenues determined by the 2022 budget law were 25 trillion rubles, but roughly extra 2.5 trillion rubles actually went into the treasury last year. Yet budget expenditures were above this increase; during the year-end press conference, Finance Minister Siluanov said that “around 30 trillion rubles” had been spent. Despite a significant discount in Ural oil (shown in the third chart), oil prices were much higher than in the previous year, and natural gas revenues were at a record level until December 5. And these are the reasons for the increase in income. The greater rise in expense was owing to, in addition to the direct (military expenditures) effect of the Ukrainian operation, the increase in government subsidies to belligerent individuals and their families, and most usually low-income people. The budget, traditionally having a surplus, ran a deficit for the first time in April and was covered for the rest of the year by Gazprom and Rosneft.

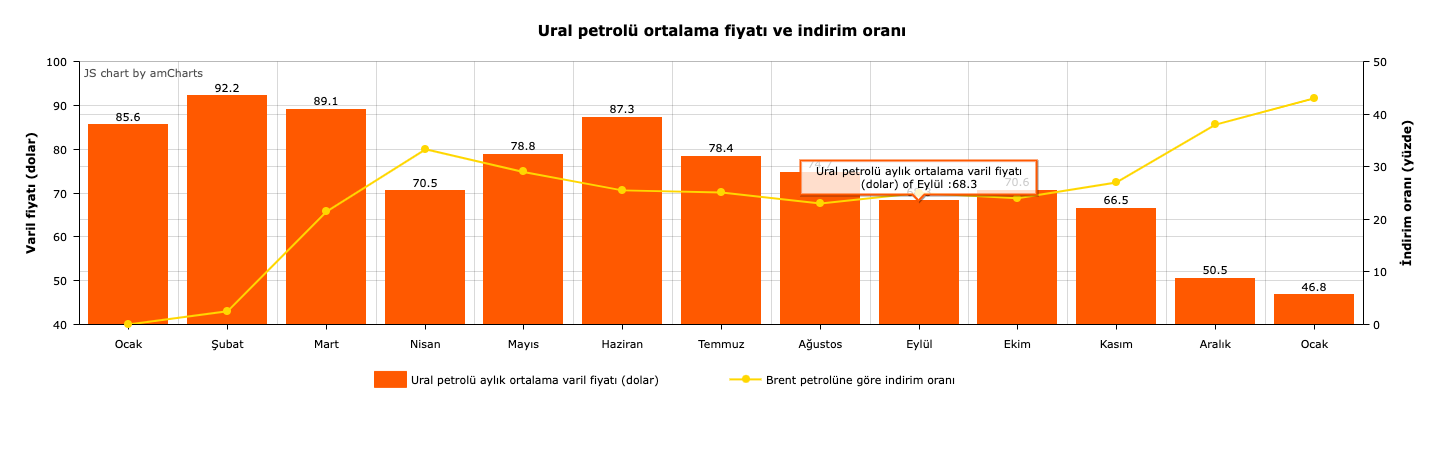

The Ministry of Finance had predicted that the price of Ural oil per barrel would be $70.1 in 2023, $67.5 in 2024, and $65.25 in 2025. However, at least for this year, it is quite unlikely that the forecast will come true. In any case, Ural oil was nearly always sold at a discount, but the price difference was generally little more than a few dollars. However, huge price differences appeared after February 24, and the average discount is roughly 30 percent from that date to the end of the year. The discount rate was relatively stable between July and October at about 20-25 percent, but it spiked sharply once the maximum price was published on December 5. Since December 30, it has fluctuated daily between 45-55% as of January 20. In addition, it is still cheaper than $60, the price cap. In contrast, the last year’s price average of Ural oil was $76.09.

The situation with natural gas is similar. According to the explanatory note in the draft budget for 2023–2025 and the official forecast for the 2024–2025 planning period, natural gas exports (total of distant and close countries) fell by 31% in 2023 compared to the previous year, landing at 142 bcm, and will average 125 bcm annually for the next two years. However, these figures should be considered too optimistic because total exports via pipelines may decrease to 90–93 bcm this year if natural gas exports to distant countries reach 70–75 bcm as expected.

According to the most reasonable estimates of the Ministry of Finance, in 2023, if the price of Ural oil per barrel stays at $50 and daily output does not surpass 10 million barrels, the government would get at least $2.1 trillion less in oil and gas revenue in 2023, and the deficit will rise to $5 trillion, instead of the anticipated $2.9 trillion (2 percent of GDP). (In addition to crude oil, other petroleum products, natural gas, coal, etc., will impact this deficit.)

Suppose Ural oil prices remain at about $62-$63 per barrel. In that case, the Ministry of Finance intends to sell yuan from the National Wealth Fund and issue bonds to cover the deficit without raising the tax burden on the bourgeoisie. Alternatively, the government decides to seize “excessive profit” on carbon and fertilizer (this is the Kremlin’s optimal solution; I looked into it further when analyzing Putin’s September 7 speech at the Eastern Economic Forum), to increase the share of the budget in the dividends of state companies (this is the “financial bloc’s” optimal solution), and to issue a new tax regulation, if it fails, or the discounted oil price drops further. The Kremlin sees raising the tax burden on the great bourgeoisie as the best way to ensure that the welfare of the people remains stable or, if feasible, is elevated by state aid. In contrast, the “fiscal bloc” would rather burden the public by increasing indirect taxes. In other words, the bourgeoisie or the people must contribute to cover the budget deficit. As a result, the “conflicting alliance” between “the potent and the impotent” continues.

Conclusion

These are, of course, just estimates anyway. But one thing is clear enough: The traditional economic paradigm (oil and gas economies) is rapidly becoming obsolete. A structural shift in the economy is inevitable. This can be done in two ways: Medium and large private capital shifts from unproductive trade or the production of raw materials for export to industrial output for the domestic market, or the state expands its role as an economic regulator.

While the first way may help in the consolidation of capitalism but given the comprador nature of private capital in Russia, it is unrealistic to assume that it will serve as the primary means. It will continue to be an alternative for the bourgeoisie is eager to fill in the lacuna created by the foreign money leaving Russia. The local bourgeoisie is flexing its muscles to seize closed and closing foreign financial and industrial institutions, so one of the reasons why the ruble has depreciated in the past month is the demand for foreign currencies for purchases. Yet, the comprador nature of capital still prevails. In the first three quarters of last year, the financial-bloc-backed bourgeoisie managed to invest abroad 2.5 trillion rubles, or 10 percent of the budget’s income. On the other hand, taking the first way for structural shift results in the bourgeoisie’s political power being consolidated and empowered, posing a challenge to Bonapartism. Finally, the greatest exporter of raw materials, the state sees no gain in income through the first way, exacerbating the structural problem. Thus, the state must serve as the driving force of structural change.