Opinion

Obligation for a structural change in Russia: How to exit from the oil-gas economy?

By analyzing the past, present, and future of Russia’s two major export commodities, I will discuss the impacts of the current developments on the budget and the inevitable need for changes in its economic strategy in this article.

First of all, one of the key notions below, “distant nations,” needs some background. Whether or not they are members of the Commonwealth of Independent States (CIS), all former Soviet countries are still regarded as close foreign countries. The rest of the world is likewise distant foreign countries. Here, we only do calculations and charts for distant foreign countries. After leaving China out, European countries constituted its overwhelming majority. Therefore, the conclusion will reflect the impacts of Western sanctions on Russia’s two primary exports and sources of budgetary income (oil and natural gas).

Let me state something upfront for the sake of the reader who is not a fan of lengthy writings. Using 2021 as a baseline, Russia will lose 35% – 40% of its oil and petroleum product exports and 50% of its natural gas exports this year. However, this is only part of Russia’s financial setback. Before the onset of the deep crisis in the first half of 2022, rising energy prices had significantly boosted the country’s income. However, the situation has now reversed, with oil and petroleum products discounted by nearly half their market price.

Natural gas

We’ll begin by explaining how the graph below was drawn, which data was utilized how and why, and how estimations were made.

In order to avoid “misjudgments, speculations, and inconsistencies,” the Federal Customs Administration (FCA) has not released information since April. Hence there is currently no official data for 2022. Gas exports to Europe (in transit via Ukraine) are projected to reach 30 bcm in 2023. At 80% capacity, gas is plummeted through Blue Stream, which equals a maximum of 16 bcm through this line. The largest volume that can be plummeted to China is between 23 and 24 bcm.

It was not disclosed how much natural gas Turkey purchased from Russia last year. However, on July 18, Yuri Ushakov, an advisor to Putin, reported that 12.8 bcm of gas (7.1 Blue Stream, 5.7 Turk Stream) had plummeted in the year’s first half. In addition, the export amounts to China and Europe (excluding “close countries” like the Baltic) are known. Based on these statistics, I estimated the gas export to Turkey at 21.70 bcm. This figure matches what Kommersant reported to the Turkish Customs Administration: 21.50 bcm.

Data from Gazprom and the FTS do not quite match. Gazprom’s export figures are always greater than FTA’s. This also held true in the year 2021. Novak reported on December 28 that Gazprom had exported 185.1 bcm to distant countries. However, according to FTS, total exports to distant countries were 170 bcm. I derived figures on the graph from Gazprom statistics. Additionally, I referred to the Central Bank’s yearly average natural gas prices. Like the FTA, the Central Bank did not integrate the averages of 2022 and afterward into its statistics. Therefore, I utilized the calculations provided by the RIA based on the ICE data as the average natural gas price in 2022: $1260.8 per mcm.

I picked two sets of prices for 2023. First, the price on December 31, 2022, is $844.3, assuming it remains relatively stable throughout the year. If scenario two plays out, temperatures in Europe will remain above seasonal norms this winter and spring, the wind will continue its record-setting speed, Brussels will strike a long-term oil deal with Qatar, relations with Algeria will improve, and the United States will replace the monopoly profit with reasonable prices. Although not all of them are realistic, I would predict that costs can be cut in half if all take place.

For 2023, I have assumed a decline in exports of 30% and a total decrease to 70-75 bcm. If this occurs, European countries will import more than twice as much natural gas from the United States as they did from Russia this year.

Novak said on December 28 that gas exports totaled 100.9 bcm last year. It is a record low. In 1990, it was 110 bcm. On January 16, Miller reported that 15.5 bcm of gas was sold to China. However, Neftegaz announced on January 2 that this figure might be appraised as 18.2 bcm due to an increase in contractual obligations. The graph relies on this second figure.

Miller also said annual gas shipments to China will reach 48 bcm by 2025. But the graph shows that even in this case, the demand from the East cannot make up for the European market loss (at least for now).

I have omitted liquefied natural gas (LNG) from the charts. This export may increase partially. Nearly 16 million tons of LNG were sent to Asia in 2022, and Europe received 15.7 million tons in total. This amount is approximately equal to 44 bcm of gas. Although this figure is not inconsequential, it is not anticipated to increase beyond this level in 2023 owing to the challenges of insurance-reinsurance in transport and tankers other than dependency on Western technology. Furthermore, it is unlikely that the rise in LNG exports would come close to replacing the 180-200 bcm of the potential capacity of the Russia-Europe pipelines before NATO destroyed Nord Stream 1 and 2.

Even by an optimistic prediction, the total demand of China, Belarus, and Turkey in 2023 would only amount to 60 bcm, less than a quarter of Gazprom’s entire supply capacity. So, this is the picture based on the most optimistic estimates: In 2021, Russia globally sold almost 240 bcm of natural gas. By 2023, however, it will only be able to ship a maximum of 45 bcm LNG and export 30 bcm via pipeline to “unfriendly” countries and 60 bcm to neutral countries.

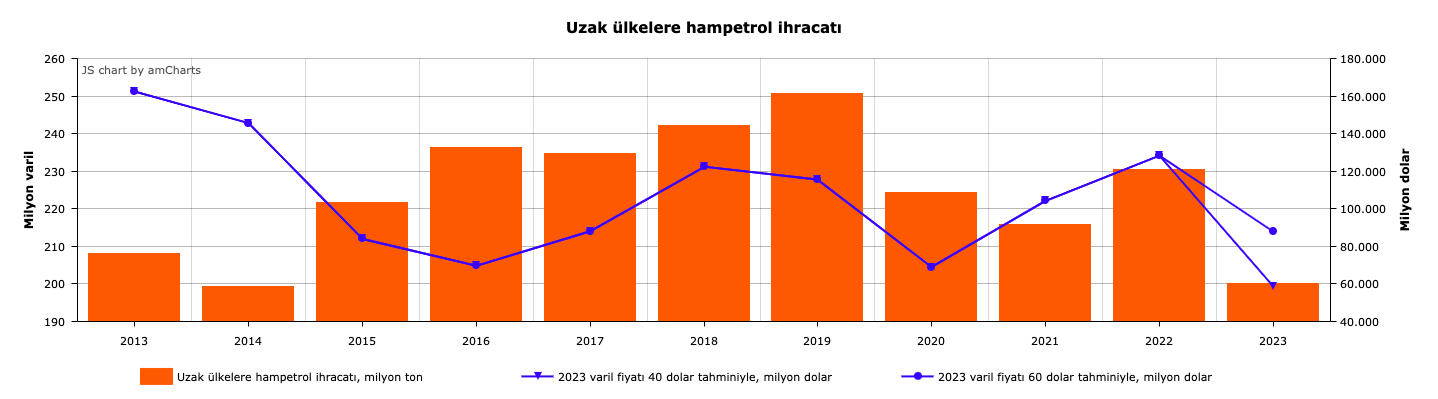

Oil

Let’s look at oil.

I will prepare the chart for the same time frame (2013-2023); however, I will be excluding the data from China, Turkey, and India. For these three reasons:

1) There are gaps in the dataset. On the bright side, it is at least evident that China had been a reliable purchaser (between 70-72 million tons) until 2022.

2) At least as of 2020, Turkish and Russian sources contradict in terms of figures for Turkey’s purchases.

3) Prior to 2022, India was not a huge market for Russian exports, but after that year, it became one of the most important hubs for Russian oil. The share of Russian oil export to India rocketed from 1% on February 24 to 18% in May. India, Turkey, Singapore, and even the United Arab Emirates (UAE) dilute Russian oil before being sold to obfuscate its origin. It is unclear, however, how they would act after Russia’s counter-sanctions go into effect on February 1. Thus, qualifying the data of these three countries will not provide useful insights.

Nevertheless, we may get insights from the figures of crude oil exports and the total income of the annual average oil price.

Like natural gas, I have completed the chart relying on the data of “distant countries” and my own estimates. Similar to natural gas, I predicted a range of $40 to $60 for the barrel price of Ural oil in 2023. These predictions align with the scenarios the Central Bank announced in May. Considering the $60 maximum price, the likely range for the price of Ural oil is between these two extremes. To “distant countries,” I projected 200 million tons of oil exports in 2023. As a result, Russia will lose 90% of its crude oil exports to Europe due to the sanctions, which may cost the country $40 to $70 billion.

I will not go into technical details of the implementation of the sanctions and embargo. Still, it’s important to know that in its broadest sense (including both land and sea traffic), it will be implemented over the course of 6-8 months. This is why the European market has not been totally lost: Bruegel, a European think tank, has shown that 75% of Russia’s oil and petroleum product exports to Europe are sent offshore, while just 25% are transported via pipeline. Germany and Poland, two main consumers, have reduced their purchases, while the Hungarian government has blocked a full ban. Orbán has ensured that the oil pipelines of Slovakia and the Czech Republic from Russia, in addition to those of Hungary, will remain open.

However, the insurance and reinsurance restrictions directly impact exports to India and China. Unless a stable solution to this issue is found (a partial solution is already available; the Russian National Reinsurance Company carries out the reinsurance), overall exports may fall further. Similar to natural gas, compensating the European market with Asia cannot happen in one day.

My estimations for potential losses are in line with these predictions as well. AlfaBank reported an expected loss of $50 billion; for Reuters, it is $40 billion to $54 billion, and for Energy Aspects, $60 billion. Increasing the amount of oil exported may improve the situation, which is feasible if the methods to circumvent the sanctions are broadened. A significant increase in the $40-$60 range for the sale of Ural oil appears unlikely.

These two charts depict a very critical scenario for 2023: Excluding petroleum products and LNG, we may expect Russia’s oil and natural gas income to be between $89.3 and $149.4 billion. This means a revenue drop of between $106 and $166 billion compared to the previous year.

Budget

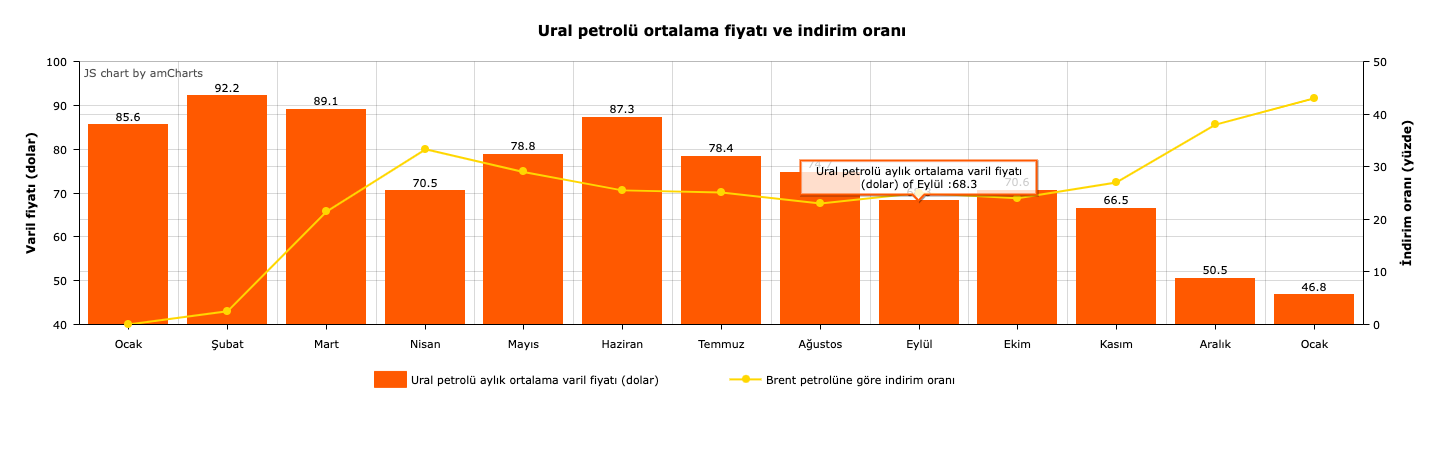

Budget revenues determined by the 2022 budget law were 25 trillion rubles, but roughly extra 2.5 trillion rubles actually went into the treasury last year. Yet budget expenditures were above this increase; during the year-end press conference, Finance Minister Siluanov said that “around 30 trillion rubles” had been spent. Despite a significant discount in Ural oil (shown in the third chart), oil prices were much higher than in the previous year, and natural gas revenues were at a record level until December 5. And these are the reasons for the increase in income. The greater rise in expense was owing to, in addition to the direct (military expenditures) effect of the Ukrainian operation, the increase in government subsidies to belligerent individuals and their families, and most usually low-income people. The budget, traditionally having a surplus, ran a deficit for the first time in April and was covered for the rest of the year by Gazprom and Rosneft.

The Ministry of Finance had predicted that the price of Ural oil per barrel would be $70.1 in 2023, $67.5 in 2024, and $65.25 in 2025. However, at least for this year, it is quite unlikely that the forecast will come true. In any case, Ural oil was nearly always sold at a discount, but the price difference was generally little more than a few dollars. However, huge price differences appeared after February 24, and the average discount is roughly 30 percent from that date to the end of the year. The discount rate was relatively stable between July and October at about 20-25 percent, but it spiked sharply once the maximum price was published on December 5. Since December 30, it has fluctuated daily between 45-55% as of January 20. In addition, it is still cheaper than $60, the price cap. In contrast, the last year’s price average of Ural oil was $76.09.

The situation with natural gas is similar. According to the explanatory note in the draft budget for 2023–2025 and the official forecast for the 2024–2025 planning period, natural gas exports (total of distant and close countries) fell by 31% in 2023 compared to the previous year, landing at 142 bcm, and will average 125 bcm annually for the next two years. However, these figures should be considered too optimistic because total exports via pipelines may decrease to 90–93 bcm this year if natural gas exports to distant countries reach 70–75 bcm as expected.

According to the most reasonable estimates of the Ministry of Finance, in 2023, if the price of Ural oil per barrel stays at $50 and daily output does not surpass 10 million barrels, the government would get at least $2.1 trillion less in oil and gas revenue in 2023, and the deficit will rise to $5 trillion, instead of the anticipated $2.9 trillion (2 percent of GDP). (In addition to crude oil, other petroleum products, natural gas, coal, etc., will impact this deficit.)

Suppose Ural oil prices remain at about $62-$63 per barrel. In that case, the Ministry of Finance intends to sell yuan from the National Wealth Fund and issue bonds to cover the deficit without raising the tax burden on the bourgeoisie. Alternatively, the government decides to seize “excessive profit” on carbon and fertilizer (this is the Kremlin’s optimal solution; I looked into it further when analyzing Putin’s September 7 speech at the Eastern Economic Forum), to increase the share of the budget in the dividends of state companies (this is the “financial bloc’s” optimal solution), and to issue a new tax regulation, if it fails, or the discounted oil price drops further. The Kremlin sees raising the tax burden on the great bourgeoisie as the best way to ensure that the welfare of the people remains stable or, if feasible, is elevated by state aid. In contrast, the “fiscal bloc” would rather burden the public by increasing indirect taxes. In other words, the bourgeoisie or the people must contribute to cover the budget deficit. As a result, the “conflicting alliance” between “the potent and the impotent” continues.

Conclusion

These are, of course, just estimates anyway. But one thing is clear enough: The traditional economic paradigm (oil and gas economies) is rapidly becoming obsolete. A structural shift in the economy is inevitable. This can be done in two ways: Medium and large private capital shifts from unproductive trade or the production of raw materials for export to industrial output for the domestic market, or the state expands its role as an economic regulator.

While the first way may help in the consolidation of capitalism but given the comprador nature of private capital in Russia, it is unrealistic to assume that it will serve as the primary means. It will continue to be an alternative for the bourgeoisie is eager to fill in the lacuna created by the foreign money leaving Russia. The local bourgeoisie is flexing its muscles to seize closed and closing foreign financial and industrial institutions, so one of the reasons why the ruble has depreciated in the past month is the demand for foreign currencies for purchases. Yet, the comprador nature of capital still prevails. In the first three quarters of last year, the financial-bloc-backed bourgeoisie managed to invest abroad 2.5 trillion rubles, or 10 percent of the budget’s income. On the other hand, taking the first way for structural shift results in the bourgeoisie’s political power being consolidated and empowered, posing a challenge to Bonapartism. Finally, the greatest exporter of raw materials, the state sees no gain in income through the first way, exacerbating the structural problem. Thus, the state must serve as the driving force of structural change.

Today, the nature of asymmetric threats is undergoing a profound transformation, with their focus shifting increasingly toward economic centers. By mid-2026, the nature of asymmetric warfare within the borders of the Russian Federation entered a qualitatively new and critical phase.

An analysis of the Ukrainian unmanned aerial vehicle (UAV) strikes carried out in July 2026 reveals a deliberate shift in targeting. Moving beyond military installations and fuel-energy infrastructure, these attacks directly targeted civilian logistics networks and critical nodes of the macroeconomic infrastructure.

The primary objective of this strategic shift is to deplete the country’s internal resources, induce insurmountable disruptions in supply chains, and exert intense psychological pressure on the civilian population.

Large-scale, coordinated strikes on the distribution centers of Wildberries—Russia’s largest e-commerce platform and part of the RVB joint venture (formed by the 2024 merger of Wildberries and Russ)—became the symbol of this new phase of home-front vulnerability. The geographic scope of these attacks, spanning an unprecedented area from the Northwestern Federal District to Southern Russia and Crimea, exposed critical gaps in national industrial risk insurance mechanisms. Furthermore, this situation sparked severe legal disputes between platform economy giants and small businesses, compelling immediate intervention from both corporate executives and senior state officials.

Tracing the multi-layered consequences of the kinetic impacts resulting from these July attacks on the state’s digital and physical economy will shape the new architecture of civilian sector security.

The zenith of the logistical terror waged by Ukraine was recorded on the night of July 24, 2026, marking the most technically complex UAV attack inflicted on Russian Federation territory since the beginning of the year. According to data from the Ministry of Defense of the Russian Federation, domestic air defense systems detected and destroyed 571 fixed-wing Ukrainian UAVs that night.

Two points have become exceptionally critical here: saturating radar fields and the military “swarm” effect. In short, this event is the clearest indication that the enemy has transitioned to a tactic of overwhelming radar systems. At the same time, the “swarm” effect generated across a vast geographic expanse aims to rapidly deplete the ammunition of anti-aircraft missile systems and expose air defense positions deep behind the front lines.

The breadth of the targeted geography attests to the unprecedented scale of the operation. UAVs were neutralized over the Belgorod, Bryansk, Kaluga, Kursk, Leningrad, Novgorod, Oryol, Pskov, Ryazan, Smolensk, Tver, Tula, and Vladimir regions, as well as over Moscow, Krasnodar, the Republic of Crimea, and the waters of the Azov and Black Seas.

Such a dense dispersion of targets across a vast territory points to an attempt to paralyze transportation and logistics arteries within Russia’s European landmass.

In parallel with the mass deployment of UAVs, missile strikes were also conducted against civilian industrial enterprises. During the same period, a missile attack on a local enterprise in the Fileyka district of Kirov resulted in outright catastrophe, leaving 6 people dead and 32 employees injured with varying degrees of severity.

Following the incident, Regional Governor Aleksandr Sokolov stated that the situation required not only the evacuation of the wounded, but also large-scale interventions such as restoring water and power supplies and auditing the security of neighboring settlements. This combined approach—employing inexpensive kamikaze drones to degrade air defenses followed immediately by missile strikes on unprotected industrial zones—presents an entirely new threat paradigm for the civilian economy.

Systematic and sequential attacks directed at the facilities of a single commercial entity completely eliminate the possibility of coincidence. The strategic, macroeconomic, and psychological factors turning civilian commercial warehouses into critical vulnerabilities for an entire state rest upon four pillars:

- Role as the central circulatory system of domestic trade: Wildberries plays a critical role in the architecture of the modern Russian economy, connecting millions of consumers with tens of thousands of SMEs. Damage to distribution centers severe supply chains, triggering localized shortages of essential consumer goods and regional inflationary spikes. The primary goal is to destabilize the domestic market and create an artificial supply vacuum.

- Immense facility footprints and defense complexity: Spanning hundreds of thousands of square meters across the nation, these hangars constitute massive targets with high radar contrast. Unlike military bases, these commercial warehouses cannot possess their own air defense systems; placing every such facility under an air defense umbrella is physically impossible without compromising frontline systems.

- Social and psychological impact: In the eyes of the public, logistics centers symbolize daily economic stability. Black plumes of smoke visible from miles away, massive fires, and civilian casualties represent a hybrid terror tactic designed to transport an atmosphere of fear deep into peaceful cities and shake the internal socio-political climate.

- Magnified radius of economic impact: Inventory consumed by flames in these warehouses generally consists of stock purchased by merchants on credit. The destruction of commodity inventories holds the potential to cause mass vendor bankruptcies, bank loan defaults, and cascading layoffs across small businesses.

The events of July 2026 mark an irreversible shift in the threat landscape facing Russian commerce and macroeconomics. Attacks directed at Wildberries hubs in regions such as St. Petersburg, Moscow, and Tambov exposed the utter vulnerability of civilian logistics infrastructure.

Deploying relatively inexpensive unmanned aerial vehicles, the enemy is capable of inflicting tens of billions of rubles in direct damage, paralyzing the supply of essential goods, and triggering an acute social crisis in which hundreds of thousands of entrepreneurs face the threat of bankruptcy. According to Russian experts, the total cost of a single fire—similar to the Kotovsk incident on July 18—can range between 50 and 100 billion Rubles ($630 million – $1.2 billion USD).

Despite its massive capital reserves, corporate business was caught unprepared for military threats. The medium-term survival of the e-commerce economy depends on the state and the private sector uniting to engineer unprecedented systemic solutions. Establishing compensation funds and introducing mandatory risk-distribution mechanisms are critical steps that must be taken.

Logistics hubs will remain open targets unless a “state program for subsidized reinsurance of military risks” is established for the critical nodes of the civilian economy. In the future, it will not suffice for large enterprises merely to pour capital into the physical protection of infrastructure; they must also deeply decentralize their logistics networks to prevent the concentration of goods and capital at single points of failure.

Dr. Ahmed Moustafa, Director & Founder, Asia Center for Studies & Translation, Egypt

For the first time since successive waves of escalation between Washington and Tehran began in recent months, an Egyptian liquefied natural gas (LNG) export facility has become a direct target.

In the early hours of Wednesday, 29 July 2026, at least one drone struck the floating storage unit Energos Winter, owned and operated by a U.S. company and sailing under the Marshall Islands flag, while it was moored at the Mediterranean port of Damietta. The impact ignited a fire that spread to a neighboring LNG carrier, GasLog Salem. Egyptian authorities confirmed that the blaze was brought under control without any reported casualties, while no group had claimed responsibility for the attack at the time of writing.

A Broader Context That Cannot Be Ignored

The incident did not occur in a vacuum. It came only hours after the United States Central Command (CENTCOM) announced that it had conducted joint strikes with Saudi forces targeting armed factions in Iraq accused of launching drone attacks against Saudi oil facilities. Tehran responded by warning against a “miscalculation,” at a time when the Middle East is still grappling with the repercussions of an earlier round of escalation that erupted on 8 July, when U.S. forces carried out strikes inside Iranian territory following an attack on a commercial vessel in the Strait of Hormuz. Iran retaliated with attacks targeting U.S. military bases in Bahrain, Jordan, Qatar, Kuwait, the United Arab Emirates, and the Sultanate of Oman.

Against this tense backdrop, Damietta appears to represent yet another link in the chain of regional escalation—but an exceptional one. For decades, Egypt has sought to keep itself removed from direct military polarization in the region, unlike several Gulf states that have increasingly become arenas of open confrontation.

At the same time, this interpretation does not entirely rule out the possibility of an indirect Israeli role, driven by hostility toward Egypt’s growing diplomatic influence in the Palestinian and Gaza files. Cairo has remained committed to advancing the two-state solution and to implementing the second and third phases of the peace roadmap agreed upon following the Sharm El-Sheikh Peace Summit last October. The Israeli government, led by Benjamin Netanyahu, has sought to obstruct these efforts. Netanyahu, who is the subject of arrest warrants issued by the International Criminal Court, is widely accused of bearing responsibility for committing genocide that, according to Palestinian authorities, have resulted in the deaths of approximately 73,000 Palestinian civilians since 7 October 2023.

Why Egypt?

Over the past two years, Egypt has steadily strengthened its position as a regional hub for liquefying and re-exporting natural gas. This growing role has been supported by its two LNG plants at Idku and Damietta, in addition to a network of pipelines linking the country with Israel and Cyprus.

This infrastructure—unmatched elsewhere in the Eastern Mediterranean in terms of combined liquefaction capacity and direct access to European and global markets—has transformed Damietta and Idku into critical gateways for Eastern Mediterranean gas, including increasing volumes of Israeli/Stolen Palestinian natural gas liquefied and re-exported through Egyptian facilities.

According to local reports, the Energos Winter alone was supplying approximately 450 million cubic feet of gas per day to Egypt’s national grid and was preparing to receive four additional cargoes during August.

This expanding role gives any attack on Egypt’s gas infrastructure significance far beyond the immediate incident itself. It threatens not only Egypt’s domestic energy supplies but also a supply chain upon which Europe has increasingly relied as part of its strategy to diversify away from Russian natural gas.

Who Was Behind the Attack? Open Scenarios

At the time of writing, no organization had officially claimed responsibility, leaving several possible interpretations.

The first scenario cautions against prematurely attributing responsibility to Iran or its regional allies. It argues that the ambiguity surrounding the incident—and the absence of any claim of responsibility—may itself be deliberate, allowing whichever actor carried out the attack to undermine Egyptian stability without incurring immediate political costs.

This possibility includes actors competing over Eastern Mediterranean energy routes, as well as local or transnational groups pursuing agendas unrelated to the U.S.-Iran confrontation. Egyptian officials themselves have adopted a notably cautious approach. Egypt’s Minister of Information warned against “rushing to accuse any party,” while a former official suggested that “certain actors are seeking to drag Egypt into the conflict,” implying that the attack may have been designed precisely to draw Cairo into a confrontation it has consistently sought to avoid.

A second scenario, Israeli Involvement or the Involvement of Israel’s Allies

This, in itself, remains a serious hypothesis that is reportedly being discussed in undisclosed investigative circles. The prevailing analyses, supported by pro-Israeli and pro-American narratives, have largely centered on suspicions directed at Iran or Iran-aligned actors within the context of the ongoing conflict, rather than at Tel Aviv. This is partly because Israel maintains an energy partnership with Egypt, making any attack on an Egyptian export terminal potentially detrimental to its own natural gas interests.

Nevertheless, this hypothesis—like all others—must ultimately be assessed in light of the findings of the official investigations, which are still underway. It is worth recalling, however, that repeated warnings have been voiced regarding the visits of Israeli Prime Minister Benjamin Netanyahu to Washington, as such visits have often been followed by heightened regional instability, as was argued after developments last December. According to this line of analysis, Netanyahu seeks to prolong the conflict with Iran in order to strengthen his domestic political position, secure his continuation in office, and advance Israel’s long-term strategic objective of neutralizing Iran and carrying out “Greater Israel.”

Within this framework, some analysts argue that there are broader efforts to weaken both Egypt and Türkey. They cite remarks attributed to a former Mossad operative during appearances on Israeli television, alleging that such a strategy would also serve to divert international attention away from the Gaza file and the question of Palestinian statehood—an issue on which Egypt has intensified its diplomatic efforts in recent days. According to this interpretation, creating indirect pressure on Egypt—the region’s most stable and secure state—could be viewed as a means of drawing Cairo into a wider regional confrontation.

A third scenario links the incident directly to the broader U.S.-Iran escalation. According to the article, The New York Times, citing two Iranian sources, reported that the attack may have been intended as a signal that global shipping and energy supplies could face deeper disruptions should Tehran or its allies choose to escalate further. The sources, however, did not identify the perpetrators or specify the launch point of the drone.

The Messages Behind the Attack

Regardless of who carried out the operation, the choice of target sends several important signals. An attack on what the article describes as the first American-owned energy asset on Egyptian soil would convey a message to Washington that not only its military installations in the Gulf, but also its economic footprint across the region, has become increasingly vulnerable.

For Egypt, which has consistently pursued a policy of strategic restraint and regional neutrality, the incident serves as a reminder that its geographic position—adjacent to some of the world’s most important energy and maritime corridors—no longer guarantees insulation from the conflicts unfolding around it.

For global markets, the attack suggests that the geographic scope of potential disruption is expanding beyond the Strait of Hormuz and the Arabian Gulf into the Eastern Mediterranean, increasing insurance premiums for shipping and critical energy infrastructure in a region long regarded as comparatively secure.

Egypt’s Official Response

The Egyptian government handled the incident with considerable caution and procedural professionalism, treating it primarily as a crisis-management operation rather than a political event.

The Cabinet confirmed that the fire had been caused by a drone attack without attributing responsibility to any specific party, emphasizing that investigations were continuing “to take all necessary measures to safeguard Egypt’s interests and national security.”

Prime Minister Mostafa Madbouly described the response as a test of the state’s crisis-management capabilities, praising emergency teams for successfully moving the burning vessels away from the port, thereby preventing what could have become a far larger disaster.

President Abdel Fattah El-Sisi addressed the incident publicly for the first time during a telephone conversation with Spanish Prime Minister Pedro Sánchez. During the call, he confirmed that the competent authorities were conducting a comprehensive investigation, warned of the dangers posed by the escalating regional situation, and stressed the importance of cooperation between Egypt and the international community to contain the crisis while adhering to peaceful solutions.

This measured diplomatic approach—avoiding direct accusations while emphasizing de-escalation—reflects Cairo’s determination not to be drawn into a broader regional confrontation despite having come under direct attack on its own territory.

Several Gulf states also expressed their full solidarity with Egypt and voiced support for its efforts to safeguard its national security and sovereignty.

The Impact on Global Energy Markets

The Damietta incident occurred at a time when global energy markets were already under considerable strain. Brent crude had been hovering around US$90 per barrel following the escalation of 8 July, while the European Title Transfer Facility (TTF) benchmark for natural gas had climbed above US$700 per 1,000 cubic meters for the first time since March.

Any additional disruption affecting an Egyptian LNG export terminal risks reinforcing this upward trend. Europe has increasingly relied on Egyptian liquefied natural gas as part of its broader strategy to diversify supplies away from Russian pipeline gas. Consequently, even a temporary interruption to Egypt’s export infrastructure could heighten market concerns over supply security.

The incident also adds to the geopolitical risk premium already factored into insurance costs for vessels operating in the Eastern Mediterranean. Higher perceived risks could translate into increased shipping and insurance costs for LNG carriers throughout the region, even if subsequent investigations conclude that the attack was an isolated event unlikely to be repeated.

What Should Be Done to Prevent Similar Incidents?

First, Egypt should further strengthen its short-range air defense capabilities and counter-drone systems around strategic energy installations along its Mediterranean coastline. This includes deploying advanced early-warning radar networks and cost-effective interception systems capable of neutralizing small unmanned aerial vehicles before they reach critical infrastructure.

Second, broader regional intelligence-sharing mechanisms should be expanded among Egypt and neighboring states—including Cyprus, Greece, and Türkiye—in recognition of the increasingly interconnected nature of Eastern Mediterranean gas infrastructure and the shared strategic importance of safeguarding regional energy corridors.

Third, given that the targeted floating storage unit is owned by a U.S. company, Washington should contribute to financing and modernizing the protection of such critical infrastructure rather than limiting its response to statements indicating that it is merely “monitoring the situation,” as the article characterizes the U.S. reaction.

Finally—and perhaps most importantly—reducing the broader cycle of regional escalation between Washington and Tehran remains the only sustainable guarantee against similar incidents in the future. Any purely technical or localized security measures can mitigate immediate risks but cannot eliminate them so long as the underlying geopolitical drivers of confrontation remain unresolved.

Conclusion

The Damietta incident serves as a stark reminder that geographic neutrality alone is no longer sufficient to shield a country that has become a pivotal node in the global energy network.

References:

1- https://www.bbc.com/news/articles/c39ez3klwmro

4- https://www.nytimes.com/2026/07/29/world/middleeast/ships-drone-strike-egypt.html

Leon Trotsky, one of the foremost leaders of the October Revolution, defined fascism as the totalitarian organization of society by monopoly capital. Magnates of large-scale monopoly capital are acutely aware that their profits cannot be safeguarded in the absence of authoritarian political power. Thus, fascism finds its bedrock of support among capitalist forces, the grand bourgeoisie, monopoly capital circles, and major landowners. We are all too familiar with the calamities fascism wrought upon the world in the era preceding the Second World War.

The post–World War II era is often commemorated as the golden age of capitalism—a period characterized by robust growth rates and low unemployment. Real wages climbed, social rights expanded, demands for a welfare state remained vibrant, and the pursuit of a social state yielded tangible results. This era ultimately met its demise in the 1970s, undone by shifts in the regime of accumulation and structural economic crises.

Today, across Europe, political parties that could virtually be characterized as the direct successors to pre-WWII fascist movements are consolidating their electoral gains. Germany, France, and Italy serve as quintessential examples. These parties weaponize poverty, unemployment, and anti-foreigner, anti-immigrant, anti-Muslim, and anti-Middle Eastern sentiments, while capitalizing on the incompetence of traditional center-right and center-left parties and taking a deeply Eurosceptic, critical stance toward the European Union. They employ caustic rhetoric against the political elites who have dominated governance for decades. Receiving endorsement from both US President Trump and Russian leader Putin, they draw substantial support simultaneously from working-class constituencies—traditionally the bedrock of the left—and from grand capital circles. While monopoly capital quietly pats these populist movements on the back, it simultaneously winks at liberal-democratic and increasingly indistinguishable social-democratic parties that champion unbridled capitalism and aggressive liberalism. Beyond France and Germany, examples abound from Italy to the United Kingdom…

The interests of grand capital, which back populist regimes and advocate authoritarian governance, also champion localization. For the erosion of the national, the public, and the collective—alongside the attenuation of the central state and the elevation of the local—works decisively to the advantage of big capital.

Why?

Because of this:

Under liberalism, the state does not regulate the market; rather, the market regulates, directs, and subdues both the state and society. In a liberal order, the state is expected to act on behalf of capital and in favor of the market—intervening in politics, society, and the law, and enacting statutory frameworks strictly to this end. The state is tasked with engineering legal and institutional arrangements for the market’s account and benefit. Society is reduced to a market-society, wherein the citizen is reimagined as a consumer, a client, and an entrepreneur. Since competition is elevated as the supreme imperative, citizens themselves must become entrepreneurial and competitive—a posture the state actively promotes and incentivizes.

According to liberals, the state bears no obligation to shield its citizens from the pitiless mechanics of the market or the ferocity of unchecked capitalism. On the contrary, the state demands and encourages that citizens establish themselves as entrepreneurial actors within the market arena. Consequently, the state aligns itself with capital, operating at its beck and call. Hence, liberalism harbors an innate preference for unorganized, non-unionized, cheap labor. Wages are suppressed; agricultural subsidies are gutted to a minimum; and strikes are banned on the flimsiest of pretexts.

Because liberalism insists that the state be sculpted, organized, and driven according to market demands—allowing the market to command and direct the state—the liberal vision of the nexus between politics and economics, as well as politics and law, is deeply fractured. In their worldview, law must operate exclusively to the advantage of capital, acting as the vigilant sentinel for the inviolability of property rights. It must dismantle every obstacle standing in the way of free trade, unbridled competition, and the free market, while swiftly and severely penalizing any force that dares to impede them. To conform to the expectations and demands of capital: this is the primary imperative required of the law.

In sum, through its championing of identity politics, its reduction of the citizen to a mere client, and its liquidation of the state’s social character in order to place public power at the disposal of capital, liberalism stands fundamentally opposed to the social, the public, and the national. This is a truth that must be firmly impressed upon left-liberals, nationalist-liberals, and conservative-liberals alike.

Defense Priorities director warns US air strategy in Middle East faces tactical limits

Macroeconomic consequences of asymmetric UAV attacks in Russia

Egypt Under Fire: What Does the Damietta Strike Mean for Global Energy Markets?

Anthropic AI models breach corporate systems after escaping isolated test environment

Morawiecki launches Rozwój Plus movement following high-profile split from Poland’s PiS

-

America2 weeks ago

America2 weeks agoUS agricultural superpower status at risk as trade wars shift global markets to Brazil

-

America2 weeks ago

America2 weeks agoUS controls $13 billion in Venezuelan oil revenues with little transparency, raising congressional concerns

-

Europe2 weeks ago

Europe2 weeks agoUS secures multi-billion-dollar energy and AI deals at Three Seas summit in Dubrovnik

-

Diplomacy2 weeks ago

Diplomacy2 weeks agoPalantir CEO Alex Karp says he would not vote for ‘pro-Russian’ AfD in Germany

-

Diplomacy2 weeks ago

Diplomacy2 weeks agoWorld Bank warns US-Iran conflict could slash global growth to 1.3% as inflation looms

-

Middle East2 weeks ago

Middle East2 weeks agoPentagon faces severe budget crunch as Middle East operational costs drain key military funds

-

Europe2 weeks ago

Europe2 weeks agoGermany accelerates African energy diplomatic push to secure natural gas and green hydrogen

-

America2 weeks ago

America2 weeks agoAIPAC cuts online donation links for Democrats after Israel aid vote